.png)

When you think of 5G, you may think of smartphones and networks, but telecom isn’t the only industry embracing 5G. Automated valuation models (AVMs) are entering their 5th generation as well!

While people have priced homes as long as they’ve been around, there have been a series of exceptional breakthroughs that have left pre-existing approaches in the past. Let’s take a look at how AVMs have evolved over time.

First Generation

In the beginning, a simple price index model used two data points to value a home: its past sales price and the House Price Index (HPI). The underlying premise was that a home was worth what it previously sold for adjusted for the net change in home prices over that time frame. Its simple approach provided a rough estimate for any previously sold property, though there are dozens, if not hundreds, of important factors it neglected. However, the principle of factoring in the changes in the overall market (e.g., a hot or a cold market) remains.

Second Generation

The price index model enjoyed a long reign until more data was digitized and hedonic models took center stage. Hedonic models break out the features of every property and then estimate the value each contributes to the home’s overall price. Over time, more and more complex regression analysis techniques were utilized to fine-tune the impact of each individual component.

While this approach was easy to understand in principle, it quickly became apparent that the price per square foot in Manhattan, Kansas varied drastically from the price per square foot in Manhattan, New York. Furthermore, the positive value of having a pool in Arizona clearly differs from its impact in Minnesota.

Not to be deterred, financial modelers quickly calculated adjustment factors and coefficients to adapt the models for varying geographies and other factors. Nevertheless, there were still too many gaps in the models for it to ever “solve” home prices.

Third Generation

The third generation was born not out of a breakthrough in modeling, but rather doubling down on the hedonic approach – think hedonic modeling on steroids. Up to this point, most regression analyses had focused on the characteristics of each individual home, but modelers soon began experimenting with additional data points, such as school quality, crime stats or proximity to public transportation. Enterprising companies began quantifying abstract concepts like walkability (e.g., Walk Score) to see what moved the needle when plugged into a model.

Furthermore, AVMs competed in a race for not only more data, but also more granular data. It was great to have a dataset on each city’s noise pollution or air quality, but infinitely more valuable if you could generate data at the zip code, or even parcel, level.

Fourth Generation

The arrival of the 2010s brought about the explosion of artificial intelligence and machine learning. The price of data storage and computing power decreased dramatically allowing more complex models to analyze ever-growing datasets. The painstakingly calculated coefficients and adjustment factors that defined the “Hedonic eras” were replaced by AI models that could optimize the weight of each attribute uniquely for each property.

Additionally, the advances in computing capabilities enabled these new AI models to be updated much more frequently. AVMs went from providing monthly value estimates to daily value estimates. This push towards real-time valuations increased the competition for data because it made it important to not only have data, but to have the most up-to-date data.

While AVM accuracy greatly improved with these new approaches, there were some side effects. The adoption of AI led to AVMs becoming more of a “black box”. It became harder to parse out how different factors were impacting each home’s valuation and AVMs became more secretive about which data sources were leveraged in their models.

Fifth Generation

All of this hard work brings us to today, the fifth generation. The latest developments are focused on addressing critics’ most frequent criticism of AVMs, the fact these models can’t “see” the property they’re valuing.

During a home visit, appraisers or real estate agents can easily verify how well a property has been maintained or the quality of updates and renovations that have been made. For an AVM though, these insights had historically remained a glaring blind spot. While creative modelers had looked to understand a home’s condition and quality by examining building permits or parsing keywords, like "luxury" or "fixer-upper", out of listing descriptions, a more comprehensive solution eluded them.

At least that was the case. In the new world of 5G, the most state-of-the-art models are leveraging a type of AI known as computer vision or image recognition to analyze property imagery to quantify a home’s quality and condition. The results are so compelling, House Canary’s recent whitepaper suggested that only “condition-informed” AVMs should be used in underwriting. In the iBuying world, OpenDoor highlighted to its investors how its “computer vision capabilities” have greatly improved its AVM performance.

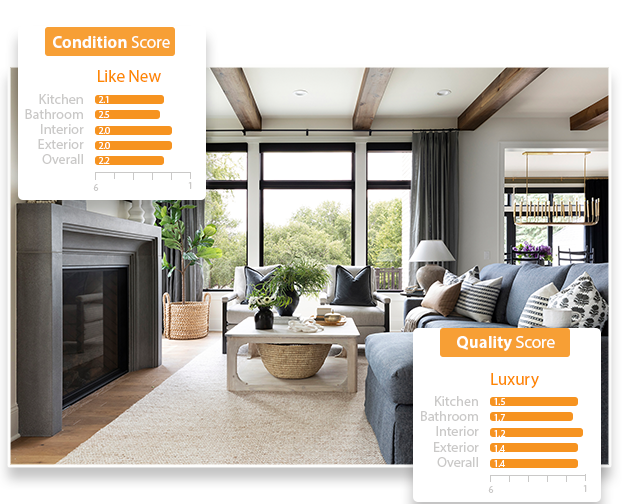

AI generated property condition and quality scores

One of the key benefits of how AI “sees” properties is that it allows for condition and quality data to be standardized in a way that is easy for models to consume. While real estate agents may always disagree on the definition of a “good condition” property, computer vision provides standardized, granular, and unbiased scores that are AVM-friendly. AI can even score and analyze the different parts of a home individually to easily understand homes in varying states of renovation (i.e. the kitchen was recently renovated but the bathrooms are 20+ years old).

What's next?

Despite the game-changing results computer vision has already had on many AVMs, it’s important to realize that we’re still in the infancy of 5G. Imagine a world where you can put a price tag on the quality of a home’s ocean view. We all know that all “views” are not created equal. Think about AVMs leveraging previously un-captured data points like kitchen layouts (e.g., galley vs. U-shaped) or colors (i.e., the impact of white cabinets vs. black cabinets). Will we be able to quantify trends?

All we know for certain is that more visual content is on the way. Companies are actively looking at how they can incentivize homeowners to upload photos of their own homes. Apple’s new RoomPlan is changing the way interior data is captured on properties. Will drone photography become the norm? Given this ever-increasing amount of data for AI to “look” at, the sky is the limit for what future AVMs will be able to achieve.

Have any additional thoughts on AVMs you’d like to share? Please reach out and let us know what you think!

comments